U.S. Added 216,000 Jobs in December, Outpacing Forecasts

The labor market ended the year with a bang.

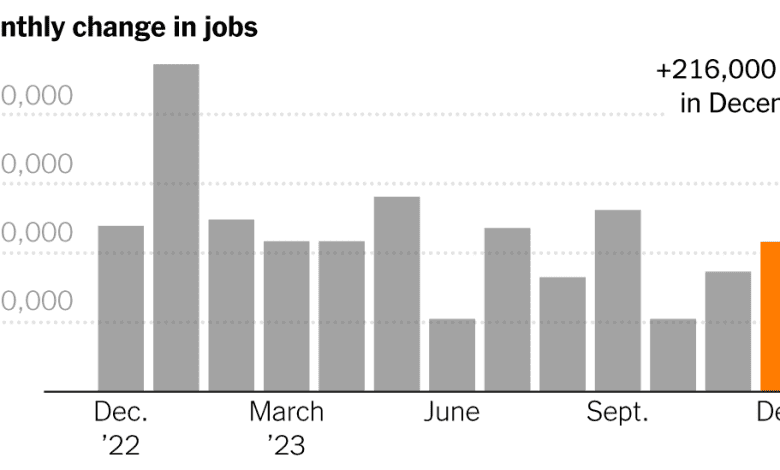

Employers added 216,000 jobs in December on a seasonally adjusted basis, the Labor Department reported on Friday, surpassing economists’ forecasts. It was the 36th consecutive month of gains.

Altogether, the U.S. economy added roughly 2.7 million jobs over the past year. That’s a smaller gain than in 2021 or 2022, during the economy’s initial resurgence from pandemic lockdowns. Yet the gains of 2023 are still stronger than those in the late 2010s.

The numbers are buoying expectations of what has been called a soft landing — in which the economy is able to avoid significant job loss while shifting into a calmer, more sustainable gear, after the disorienting volatility that began with the arrival of Covid-19 roughly four years ago.

Many experts caution that data for December is notoriously hard to calculate in any year because of the hiring churn caused by the holiday season.

The unemployment rate, based on a survey of households, was unchanged at 3.7 percent.

Average hourly earnings for workers — a common measure of wage gains — rose 0.4 percent from the previous month and were up 4.1 percent from December 2022, an unexpectedly strong increase that may help improve worker sentiment if inflation continues to ease.

Layoffs remain near record lows, beneath prepandemic levels.

The resilience of job and wage gains is all the more remarkable in light of the Federal Reserve’s aggressive series of interest rate increases in the past couple of years.

As ever, though, threats to overly sanguine outlooks abound.

Heading into 2023, over 90 percent of chief executives surveyed by the Conference Board said that they were expecting a recession. The resilience of the economy has prompted plenty of business leaders to readjust their overall expectations and, in many cases, their hiring plans. Some feel that the full effect of those heightened borrowing costs may still be lurking around the bend.

Kathy Bostjancic, chief economist at the insurance giant Nationwide, projects that the economy will experience at least a moderate recession this year.

“We already see signs that cyclically sensitive sectors of the economy are significantly pulling back on adding workers to their payrolls,” she wrote in a note outlining her annual outlook. “We foresee moderate job losses unfolding by mid-2024. The unemployment rate should rise to around 5 percent later in 2024.”

Services like health care, social assistance work and state and local governments led the way in December job gains, but other previously hot sectors such as transportation and warehousing either lost jobs or edged only slightly upward, a possible indicator of cooling.

And the labor force shrank by almost 700,000 workers, according to the government’s survey. That was unwelcome news after steady labor force growth for much of 2023.

A tension over the past year has been the tug between continually improving overall data about the economy and households’ frustration with higher prices and other lingering pandemic shocks. For nearly two years, inflation was outstripping wage gains. That balance has shifted in recent months, however, and is projected to continue.

The closely watched University of Michigan Consumer Sentiment Index climbed for much of the year, but by December it was still lower than it has been 83 percent of the time since 1978, a period that has included shocks and slumps that, on paper, look worse.

That disconnect has hurt voter opinions of President Biden’s handling of the economy, surveys show.

Geopolitical chaos has upended previous predictions that inflation would fall as the economy holds steady and that supply chains would calm. In 2022, the Russian invasion of Ukraine caused the prices of oil and a wide range of food and energy commodities to soar, sometimes doubling or more.

Last year largely provided a lull in new disruptions. But conflagrations in the Middle East have broadened since fall, threatening key international trade routes. Maersk, the goliath company in international shipping, has announced that for the foreseeable future it will keep container ships away from the Red Sea, where drone and missile attacks against merchant ships have picked up in recent weeks.

As a result, the cost to ship goods from Asia to northern Europe surged by roughly 170 percent since December. For now, however, oil prices have remained mostly unaffected. And analysts on the optimistic side of U.S. economic debate are largely sticking to their guns.

Joseph Brusuelas, the chief economist at RSM, a consulting firm, says that in his view, inflation will continue to ease, “which will bolster domestic household balance sheets and boost consumption in the year ahead.”

Art Papas, the chief executive of Bullhorn, a staffing and recruitment agency based in Boston, said “there is a lot of pent-up demand” among his customers — midsize and large companies — as they anxiously wait for a green light on further hiring and investment.

“It feels like we’re in this weird state of balance,” he said, “which I’ve never seen before.”